On February 12, City CFO Robert Cortinas gave a presentation to the Financial Oversight and Audit Committee on the current state of the City’s debt.

The City owes $843,920,00 in general obligation bonds, $411,980,000 in certificates of obligation, $55,430,000 in special revenue bonds (for the construction of the Ballpark), and $16,695,000 in revenue bonds (for the airport).

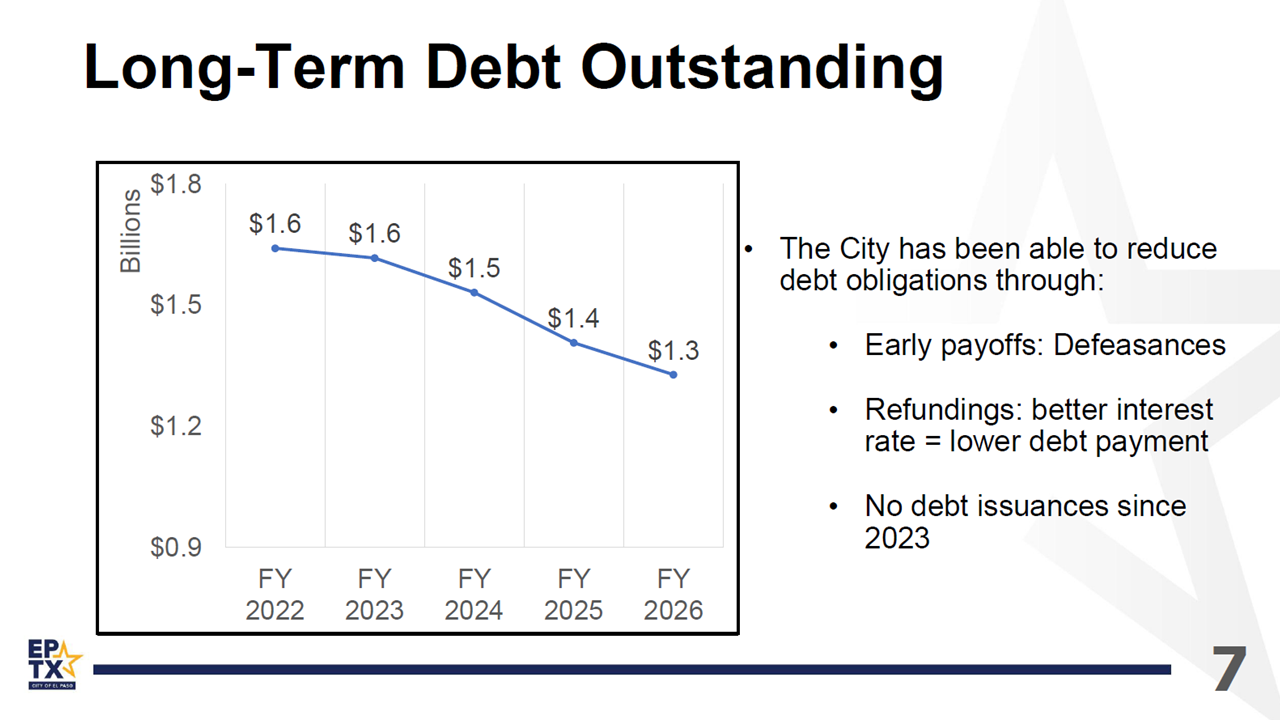

Thus, the total principal owed is $1,328,025,000, down from more than $1.6 billion in FY 2023.

According to Cortinas, the debt principal decreased by $300 million because of early payoffs (including $53 million defeased from the failed Arena project), bond refundings for a better interest rate, and the fact that no debt has been issued since FY 2023.

Cortinas points out the City must issue $472.2 million in GO debt from the voter-approved Public Safety Bond and the Community Progress Bond over the next 8 years. He currently recommends that $139.7 million be issued in FY 2027, $152 million in FY 2028, $120 million in FY 2029, and $82.2 million in FY 2030-33.

All of that will place upward pressure on our debt service tax rate, which will increase from $0.214 per $100 of valuation to $0.226 in FY 2030, or 5.6%.

Currently the City’s bond ratings indicate a “very low credit risk,” with a AA from both S & P and Fitch.

Cortinas is a skilled CFO and deserves kudos for finding creative ways to reduce the City’s debt but, of course, he does not set spending policy. That is the job of the Mayor and City Council, who until FY 2023 were on a spending binge for the record books.

Our current City Council voted to increase our City property tax by 4.3% in August but, as of yet, has not increased our debt load. That will change next year when the City begins to issue voter-approved GO debt nine figures at a time, and that will drive up our taxes.

Of course, no one can predict the fiscal impact if our City moves forward with a major bond in support of the Debt Plaza or some other boondoggle.